Most people avoid thinking about income tax until the deadline is right around the corner. Then it’s a mad rush — gathering documents, panicking over which regime to pick, and hoping nothing goes wrong on the portal. It doesn’t have to be that way. Understanding how income tax works in India is genuinely simpler than it looks, especially now that the government has made the new tax regime more generous and the filing process more streamlined. With the ITR filing deadline of July 31, 2026 fast approaching for salaried individuals, and the landmark Income Tax Act 2025 having taken effect from April 1, 2026, this is the perfect moment to get clear on everything — slabs, deductions, deadlines, and smart filing tips — all in one place.

What Is Income Tax?

Income tax is a direct tax the Government of India charges on the money you earn during a financial year. It applies to salary, business profits, rent, capital gains, interest and any other income source. The tax follows a progressive slab structure — meaning the more you earn, the higher your tax rate and taxpayers can currently choose between two regimes: the new (default) regime and the old (optional) regime.

The current filing cycle covers FY 2025-26, which means income earned between April 1, 2025, and March 31, 2026. The assessment year is AY 2026-27 and this is what your ITR this season is for. Importantly, even though the new Income Tax Act 2025 officially replaced the Income Tax Act 1961 from April 1, 2026, the AY 2026-27 filing is still governed by the old 1961 Act since the income relates to the period before April 2026. Tax professionals, financial advisors and educational platforms such as lslmarketing often emphasize understanding this distinction because it helps taxpayers avoid confusion when filing their returns and interpreting the latest tax regulations.

Income Tax Slabs for FY 2025-26: New vs Old Regime

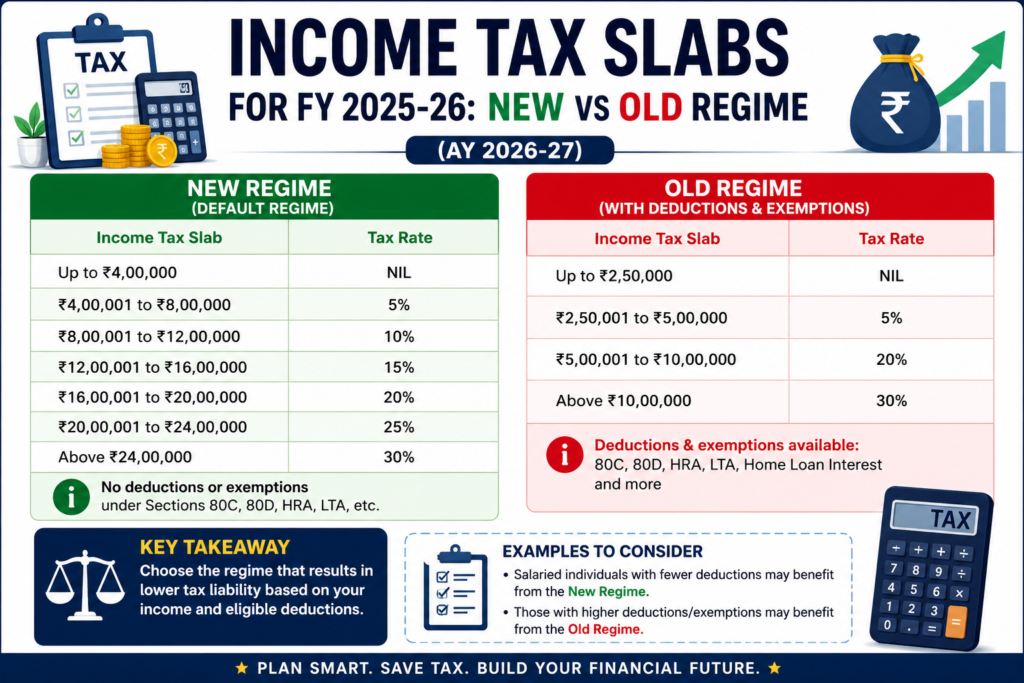

New Tax Regime (Default)

Budget 2025 brought the biggest overhaul in years to the income tax slabs under the new regime and Budget 2026 kept them unchanged. Here’s what applies for AY 2026-27:

- Up to ₹4 lakh — Zero tax

- ₹4 lakh to ₹8 lakh — 5%

- ₹8 lakh to ₹12 lakh — 10%

- ₹12 lakh to ₹16 lakh — 15%

- ₹16 lakh to ₹20 lakh — 20%

- ₹20 lakh to ₹24 lakh — 25%

- Above ₹24 lakh — 30%

Thanks to the Section 87A rebate of ₹60,000, individuals earning up to ₹12 lakh under the new regime pay zero tax. Salaried employees also receive a standard deduction of ₹75,000, which effectively makes income up to ₹12.75 lakh completely tax free. Nearly 1 crore additional taxpayers moved to zero tax liability because of these changes — a significant, real-world relief for India’s middle class.

The new regime is the default for everyone. If you don’t explicitly choose the old regime at the time of filing, you’re automatically placed under the new one.

Old Tax Regime (Optional)

The old tax regime has remained untouched in both Budget 2025 and Budget 2026. It offers a basic exemption limit of ₹2.5 lakh for general taxpayers, ₹3 lakh for senior citizens (60–80 years), and ₹5 lakh for super senior citizens (above 80 years). Its rates are higher in the middle brackets, but it allows a wide range of income tax deductions that can dramatically reduce your taxable income if you’ve invested well. Discussions around fiscal planning and revenue distribution by bodies such as the sixteenth finance commission have further highlighted the importance of understanding tax structures, deductions, and exemptions when making long term financial decisions.

The old regime makes more sense for you if your combined eligible deductions under 80C, HRA, home loan interest, 80D, and NPS cross approximately ₹3.5 to ₹4 lakh. Below that threshold, the new regime’s generous slab structure and zero tax benefit almost always wins. Always run the numbers using an income tax calculator before deciding — the Income Tax Department’s own portal has a free comparison tool built in.

Key Income Tax Deductions Under the Old Regime

If you’re considering the old regime, these are the income tax deductions that can genuinely bring your taxable income down:

Section 80C (up to ₹1.5 lakh) covers the most common investments — PF contributions, PPF deposits, ELSS mutual funds, NSC, 5-year FDs, life insurance premiums, and children’s tuition fees. Most salaried individuals already hit a large chunk of this limit through their employer’s PF deduction without even trying.

Section 80D (up to ₹25,000 to ₹1 lakh) covers health insurance premiums. If your parents are senior citizens, their premium alone allows a deduction of ₹50,000 — in addition to ₹25,000 for your own family’s coverage.

Section 24(b) — Home Loan Interest (up to ₹2 lakh) is one of the largest individual deductions available. If you’re servicing a home loan on a self occupied property, this deduction alone can make the old regime significantly more attractive.

HRA Exemption applies to salaried employees living in rented accommodation. The exemption is calculated based on actual HRA received, rent paid over 10% of basic salary, and city category — 50% of basic salary for metro cities, 40% for others.

Section 80CCD(1B) — NPS (additional ₹50,000) allows a deduction above and beyond the ₹1.5 lakh Section 80C limit for NPS contributions. For someone in the 30% tax bracket, this alone saves ₹15,000 in tax and many salaried professionals overlook it entirely.

Income Tax Return Filing in 2026: Deadlines You Must Know

The income tax return filing deadlines for AY 2026-27 are staggered this year — a first introduced by Budget 2026 — so it’s important to know which category applies to you.

July 31, 2026 is the last date for salaried individuals and those filing ITR-1 or ITR-2. This covers the majority of working professionals and is the most critical date to remember.

August 31, 2026 applies to non-audit businesses and professionals filing ITR-3 or ITR-4. This extension gives freelancers, consultants and small business owners an extra month compared to previous years.

October 31, 2026 is the deadline for companies and businesses that require a tax audit.

December 31, 2026 is the belated return window for anyone who misses their original deadline. Filing a belated return, however, comes with a late fee of up to ₹5,000 under Section 234F and interest under Section 234A. It also means losing the right to carry forward certain losses — a real cost worth avoiding.

March 31, 2027 is the last date to file a revised return for AY 2026-27, if you discover errors after your original filing — such as missed deductions or incorrect bank details.

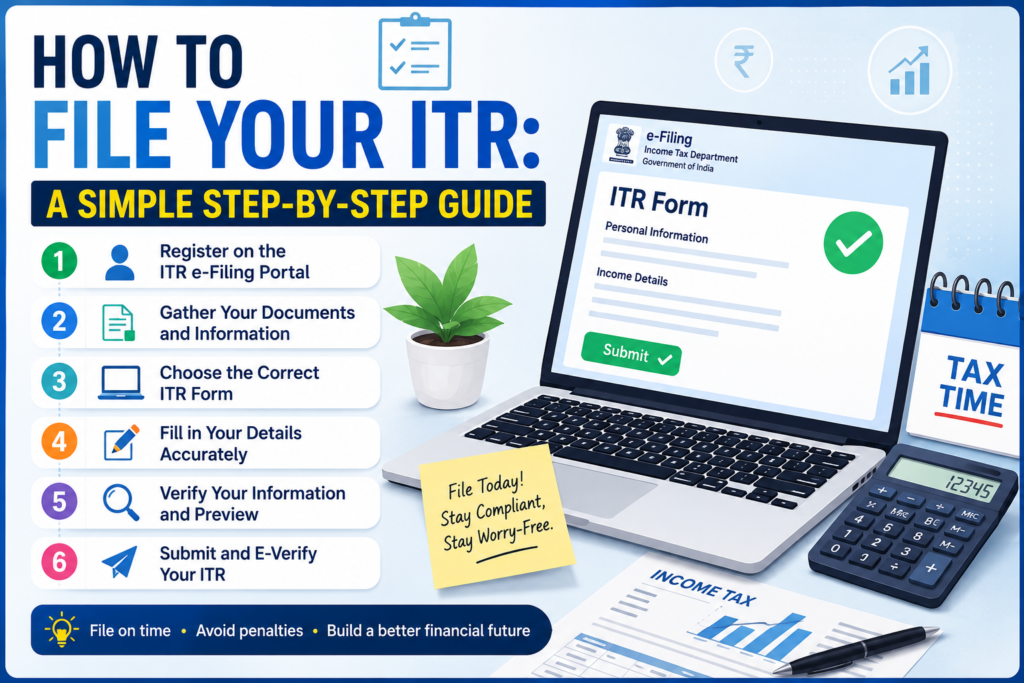

How to File Your ITR: A Simple Step-by-Step Guide

Filing online through the Income Tax e-filing portal is straightforward once you know the steps:

- Collect your documents — Form 16 from your employer, bank interest certificates, investment proofs, rent receipts for HRA, home loan interest certificate if applicable.

- Log in at incometax.gov.in using your PAN and password. First-time users register with their PAN.

- Compare regimes using the built-in tax calculator on the portal. Enter your income and deductions to see your liability under both regimes side by side.

- Choose the correct ITR form — ITR-1 works for most salaried individuals with salary income, one house property, and income from other sources up to ₹50,000. Those with capital gains or multiple properties need ITR-2.

- Verify pre-filled data — The portal auto-fills much of your salary and TDS data from Form 26AS. Cross-check it against your Form 16 before proceeding.

- Enter deductions applicable to your chosen regime — 80C, HRA, home loan interest, etc. for the old regime; or confirm the standard deduction for the new regime.

- Submit and verify — After submission, verify your return instantly via Aadhaar OTP or net banking. An unverified return is treated as invalid, so this step is mandatory.

Tips for Smarter Tax Planning

Planning your taxes in April rather than March makes an enormous difference — both financially and mentally. Start by deciding your regime early in the financial year, because investments made through the year (PPF, ELSS, NPS) need to be planned around that decision.

Always check your Form 26AS before filing. This document reflects all TDS deducted against your PAN and any mismatch between it and what you declare can trigger a notice from the IT Department. Most mismatch issues come from overlooked FD interest or freelance TDS — simple to fix if caught early, stressful if flagged later. Financial awareness is becoming increasingly important for entrepreneurs and professionals involved in a Top Trending Business in India, where accurate tax reporting and compliance play a crucial role in maintaining smooth business operations and avoiding unnecessary legal complications.

Use an income tax calculator to run your numbers honestly. Don’t assume the new regime is always better and don’t assume the old regime is better just because you’ve always filed that way. Run the actual calculation, every year, because your income and investments change.

Common Mistakes to Avoid

Not declaring all income sources is the most common error. Bank interest, FD interest, rental income from a second property, and freelance payments all need to be declared — the IT Department receives data directly from banks and employers.

Forgetting to verify the return after filing is a surprisingly common mistake. An unverified return is not a filed return. Always complete e-verification within 30 days of submitting.

Choosing the wrong ITR form leads to a defective return notice. If you’ve sold mutual funds or shares during the year, you need ITR-2, not ITR-1 — even if the gain is small.

Missing the July 31 deadline to save a few days costs more than it saves. Filing a belated return means losing carry-forward benefits on losses, paying a ₹5,000 late fee, and interest charges. The few days of procrastination simply aren’t worth it.

Conclusion: File Early, File Right

The income tax system in India in 2026 is more taxpayer-friendly than it has been in years — a ₹12 lakh zero-tax threshold under the new regime, clear staggered deadlines, and a simplified portal that does much of the pre-filling for you. There are fewer excuses than ever to delay or get it wrong.

Pull out your Form 16, open an income tax calculator, decide your regime, and file well before July 31. A few hours of effort now saves you weeks of stress and potentially thousands of rupees in penalties later. The government has made it easier. The rest is up to you.

Frequently Asked Questions (FAQs)

1. What is the income tax return filing last date for salaried individuals in 2026?

The last date for salaried individuals filing ITR-1 or ITR-2 is July 31, 2026 for FY 2025-26 (AY 2026-27). Non-audit businesses and professionals have until August 31, 2026. Missing these dates attracts a late fee of up to ₹5,000 under Section 234F.

2. How much income is tax-free under the new regime for AY 2026-27?

Individuals earning up to ₹12 lakh pay zero income tax under the new regime due to the Section 87A rebate of ₹60,000. Salaried individuals get an additional standard deduction of ₹75,000, making income up to ₹12.75 lakh effectively tax-free.

3. Which income tax regime is better — new or old in 2026?

The new regime is better for those without large eligible deductions. The old regime works better if your combined deductions under 80C, HRA, home loan interest, 80D, and NPS exceed approximately ₹3.5–₹4 lakh. Use a free income tax calculator on the IT portal to compare both regimes based on your actual numbers before filing.

4. What are the most important income tax deductions in the old regime?

The key deductions include Section 80C (up to ₹1.5 lakh for PF, PPF, ELSS, insurance), Section 80D (health insurance up to ₹25,000–₹1 lakh), Section 24(b) (home loan interest up to ₹2 lakh), HRA exemption for rent paid, and Section 80CCD(1B) for NPS (additional ₹50,000 beyond 80C).

5. What happens if I miss the July 31, 2026 income tax deadline?

You can file a belated return until December 31, 2026, but you’ll pay a late fee of up to ₹5,000 under Section 234F and interest under Section 234A. You’ll also lose the right to carry forward capital and business losses. A revised return to correct errors can be filed until March 31, 2027.

Leave feedback about this